Should I Open A Roth Ira With Robinhood

Hey there, future millionaire (or at least, future person with a slightly less stressful retirement)! So, you’ve been hearing the whispers, maybe even the shouts, about Roth IRAs. They sound fancy, right? Like something only super-organized, adulting pros with spreadsheets for brains know about. But guess what? They’re actually pretty darn cool, and you don’t need a degree in finance to get one. And then, the name Robinhood pops up. You’re probably thinking, "Wait, isn't that the app where I can buy stocks with my spare change and pretend I'm Gordon Gekko for a day?" Yup, you got it! So, the big question on your mind is likely: "Should I open a Roth IRA with Robinhood?" Let's break it down, friend, without any stuffy jargon or confusing charts. We’re just gonna chat, like we’re grabbing coffee (or, you know, scrolling through TikTok).

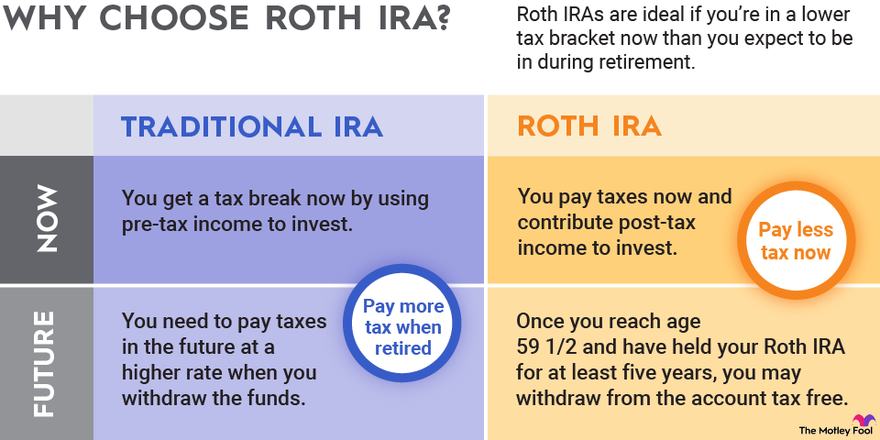

First off, let’s get our bearings. What is a Roth IRA, anyway? Think of it as a special savings account for your retirement. The "IRA" part just stands for Individual Retirement Arrangement. Not too scary, right? The "Roth" part is actually named after a senator, but the important bit for us is how it works. Unlike a traditional IRA, where you get a tax break now on the money you contribute, with a Roth IRA, you pay taxes on your contributions today. Sounds counterintuitive, I know. Why would you want to pay taxes earlier? Well, here’s the magic: when you retire, all your withdrawals – the money you put in and all the earnings it made over the years – are completely tax-free. Mind. Blown. It’s like a tax-free vacation for your future self! Imagine, sipping on a piña colada on a beach somewhere, and Uncle Sam isn’t taking a bite out of your hard-earned retirement fund. Sweet!

Now, let’s talk about Robinhood. You probably know them for their super-user-friendly app and the ability to buy and sell stocks, ETFs, and even crypto without paying commissions. They made investing feel accessible to a whole new generation. And yes, they do offer Roth IRAs. So, the question becomes: is Robinhood a good place to open your Roth IRA? This is where we dig a little deeper, beyond the flashy interface and the confetti that pops up when you make a trade.

One of the biggest draws of Robinhood is its simplicity. If you’re new to investing, or if you find traditional brokerage platforms a bit overwhelming with all their options and sub-menus, Robinhood can feel like a breath of fresh air. The app is designed to be intuitive. You can see your investments clearly, make trades with a few taps, and it doesn’t feel like you need a decoder ring to navigate. For someone who’s just dipping their toes into the world of retirement savings, this can be a huge plus. Less intimidation means more action, and that’s what we want when it comes to building your future nest egg. No one wants to feel like they’re trying to solve a Rubik’s cube while also trying to save for the next 40 years, right?

Another big selling point for Robinhood is its commission-free trading. This is a pretty standard feature for most online brokers nowadays, but it’s still a win for your wallet. Every dollar you save on fees is a dollar that can go towards growing your investments. With a Roth IRA, your goal is to have that money grow over a long period, so minimizing fees can make a surprising difference over decades. Think of it like this: if you’re buying a pizza and the restaurant charges you an extra dollar for a tiny sprinkle of oregano, you’d probably skip it, right? Fees are kind of like that oregano sprinkle, but for your investments.

However, and this is a big "however," Robinhood isn't without its criticisms. You might remember some of the controversies surrounding the platform, particularly during certain market events. Some users have expressed concerns about the platform's reliability during high trading volume, and there have been questions about their customer support. Now, it's important to say that Robinhood has been working to address these issues and improve their services. But it's something to be aware of. If you’re the type who wants 24/7 access to a human being who can answer your deepest investment queries at 3 AM, Robinhood might not be your absolute best bet for customer service. Their customer support is primarily online and app-based.

So, what does this mean for your Roth IRA decision? Well, if you’re looking for a straightforward, easy-to-use platform to get your Roth IRA started and you’re comfortable with a mostly digital customer service experience, Robinhood could definitely be a contender. It’s fantastic for beginners who want to invest in common ETFs (Exchange Traded Funds) or individual stocks within their Roth IRA. Think of it as a great entry point. You can easily set up recurring contributions, which is a super smart way to consistently add to your retirement savings. Little and often, that’s the mantra!

But, and there’s always a "but" when we’re talking about money, right? If you’re someone who plans on needing a lot of hand-holding, wants access to a wide array of investment products beyond stocks and ETFs (like mutual funds, bonds, or CDs), or if you prioritize a robust, personal customer service experience, you might want to look at other brokers. Many other brokerage firms offer Roth IRAs with more research tools, more investment options, and a more traditional customer service setup. Some even offer financial advisors you can talk to.

Let's get a bit more specific. What can you actually do with a Roth IRA on Robinhood? You can invest in individual stocks, ETFs, and options (though options trading can be a bit more advanced and risky, so tread carefully there, my friend!). This is great if you have a clear idea of which companies or sectors you want to invest in. For example, you could open a Roth IRA and decide to put all your contributions into an ETF that tracks the S&P 500. This is a popular and generally well-diversified strategy. Or, you could pick a few individual tech stocks you’re really excited about (just remember, past performance is no guarantee of future results – that’s the grown-up way of saying “don’t put all your eggs in one very shiny, possibly wobbly, basket”).

The contribution limits for IRAs are set by the IRS, and they change annually. For 2023, you can contribute up to $6,500 if you're under 50, and $7,500 if you're 50 or older (that’s the "catch-up" contribution). These limits apply to the total you contribute across all your IRAs (so if you have a traditional IRA somewhere else, that limit applies to both combined). Robinhood makes it easy to track how much you’ve contributed towards your annual limit within their app. It’s like a little progress bar for your financial future!

Now, let’s talk about the why behind the Roth. We already covered the tax-free withdrawals in retirement, which is a pretty sweet deal. But there are other perks. Because you pay taxes on your contributions now, your money grows unhindered by annual income taxes. This is especially beneficial if you expect to be in a higher tax bracket in retirement than you are now. For younger folks, this is often the case! You’re likely earning less now than you will be when you’re at the peak of your career, so paying taxes now at a lower rate makes a lot of sense. Plus, with a Roth IRA, you can withdraw your contributions (not the earnings) at any time, for any reason, without penalty or taxes. This can be a nice little emergency fund backup, though it's generally best to leave your retirement money to grow!

So, to sum up the Robinhood Roth IRA situation:

The Good Stuff (Why Robinhood Might Be Your Jam):

- Super Easy to Use: If you like clean interfaces and simple navigation, Robinhood excels here.

- Commission-Free Trading: More of your money stays invested. Woohoo!

- Great for Beginners: Lowers the barrier to entry for starting your retirement savings.

- Accessible: You can manage your Roth IRA right from your phone.

- Good for Stocks and ETFs: If that’s your primary investment strategy within your Roth, it’s straightforward.

Things to Consider (Where Other Brokers Might Shine):

- Customer Support: If you crave direct, personal assistance, Robinhood's support model might not be ideal.

- Limited Investment Options: If you want more complex investments like mutual funds or bonds, you might need to look elsewhere.

- Platform Reliability: While improving, past concerns about outages during high volatility are something to keep in mind.

- Research Tools: If you’re a deep-dive researcher, other platforms might offer more sophisticated tools.

Ultimately, the decision is yours, my friend! If you’re a digital native who’s comfortable with app-based services and you’re primarily interested in investing in stocks and ETFs within your Roth IRA, then Robinhood is a perfectly viable option to consider. It’s a great starting point to get you on the path to retirement security. Think of it as the friendly, approachable gateway drug to sensible investing. No pressure, just possibilities!

However, if you’re someone who prefers a more traditional brokerage experience, wants a wider range of investment choices, or highly values direct customer support, then it’s definitely worth exploring other platforms. There are tons of fantastic options out there, each with their own unique strengths. Do a little comparison shopping! Look at Vanguard, Fidelity, Charles Schwab – these are the seasoned veterans of the investing world, and they also offer excellent Roth IRA options.

The most important thing is not where you open your Roth IRA, but that you open one and start contributing. Seriously, time is your greatest asset when it comes to retirement investing. The earlier you start, the more time your money has to grow through the magic of compound interest (which is basically like a snowball rolling down a hill, getting bigger and bigger). So, whether you choose Robinhood, or one of its many competitors, take that first step. You’ll be thanking yourself years from now, probably while enjoying a tax-free retirement vacation!

So, go forth! Explore your options. Open that Roth IRA. And remember, even the most epic financial journeys start with a single, brave click. You’ve got this, and your future self is already giving you a high-five and a virtual thumbs-up. Now go make those financial dreams a reality!