Can A Retired Teacher Collect Social Security

Hey there, fellow humans navigating this wonderful, sometimes wacky, thing called life! Let's chat about something that’s on a lot of minds, especially for those who’ve spent years shaping young minds: retired teachers and Social Security. You might be picturing a seasoned educator, chalk dust still clinging to their tweed jacket, wondering if they can finally kick back and enjoy those hard-earned Social Security benefits. The short answer? Usually, yes! But, like a surprise pop quiz, there are a few little twists and turns to understand.

Think of it this way: after pouring your heart and soul into teaching, you’ve definitely earned a break. You’ve juggled lesson plans, endured endless parent-teacher conferences (sometimes with parents who were almost as challenging as the students!), and celebrated every single "aha!" moment. That’s a big deal! So, the idea of Social Security supplementing your retirement income is a pretty sweet prospect. It's like finding that perfect parking spot right out front when you're already running late – pure bliss!

Now, let’s get down to the nitty-gritty, but don't worry, we're keeping it light. The main thing that affects whether a retired teacher can collect Social Security is how they were paid during their teaching career. Did they contribute to Social Security directly, or did their salary come from a system that didn't involve Social Security contributions?

The Two Main Paths

Imagine you're at a delicious buffet. There are a couple of main serving stations, and which one you choose (or, in this case, which system your employer used) makes all the difference for your Social Security pudding.

Path 1: You Paid Into Social Security (Hooray!)

This is the most common scenario for teachers in many parts of the United States. If your school district, university, or other educational institution was paying into Social Security on your behalf, then congratulations! You’ve been building up your Social Security credits with every paycheck. This is like depositing money into your piggy bank over the years. When you retire, you’ll be eligible to collect those benefits, just like most other workers.

Think of Mrs. Gable, who taught third grade for thirty years in a suburban school district. Her paychecks clearly showed Social Security deductions. When she retired, she applied for her Social Security retirement benefits, and everything went smoothly. She’s now enjoying her retirement, perhaps visiting her grandkids more often, and her Social Security is a lovely bonus that helps her do just that. It’s the reward for years of dedication!

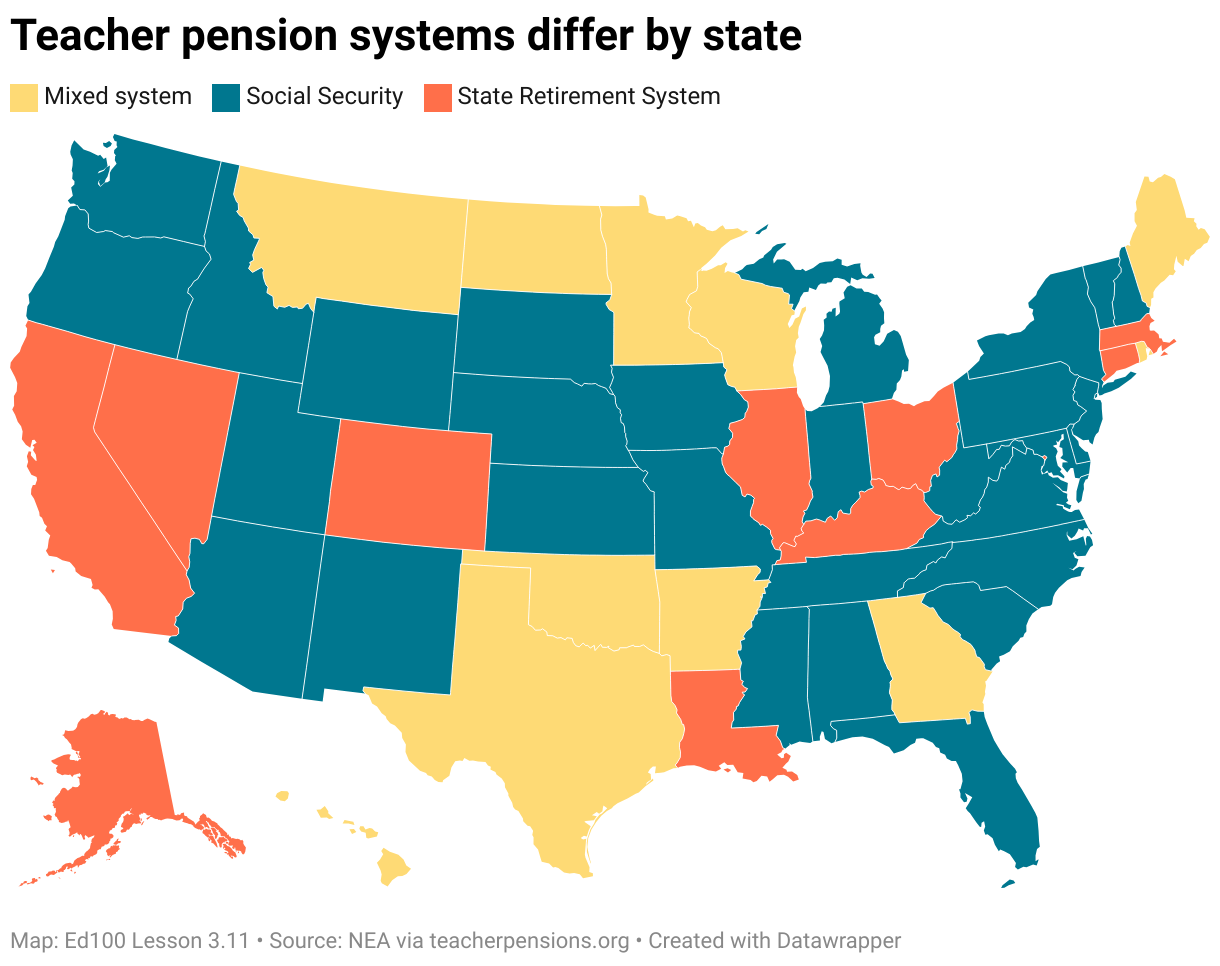

Path 2: You Were in a Special Retirement System (Hmm, a Little Different)

This is where things can get a tiny bit more complex. Some states, and even some specific school systems (especially those that are older or have a long history of independence), have their own pension plans that don’t include Social Security contributions. If you were a teacher in one of these systems, you might not have been paying into Social Security directly. This is like choosing a different buffet line that doesn't have the Social Security pasta, but it has its own delicious offerings – a pension!

Let's meet Mr. Henderson. He taught history at a prestigious private academy for 35 years. The academy had a fantastic pension plan, so generous that teachers didn’t contribute to Social Security. When Mr. Henderson retired, he started receiving his pension. But, because he never paid into Social Security, he wouldn't automatically be eligible for Social Security retirement benefits based on his teaching career alone.

The "Windfall Elimination Provision" and "Government Pension Offset"

Now, this is where the terms might sound a bit like a law textbook, but let’s break them down with a smile. These are two important rules that can affect retired teachers who have pensions from jobs where they didn't pay Social Security.

The Windfall Elimination Provision (WEP):

Imagine you worked a little bit in a job where you did pay into Social Security earlier in your life, maybe during college or a summer job, and then you spent most of your career teaching in a system without Social Security. The WEP is designed to prevent you from getting an overly generous Social Security benefit because of that brief period of contributions. It basically adjusts your Social Security benefit to reflect that you have another significant pension.

Think of it like this: you have two ovens, one that bakes cookies really fast (your pension) and another that bakes them a bit slower (your Social Security). The WEP ensures that you don’t end up with an absurdly huge pile of cookies (benefits) just because you used the fast oven for a while and then the slow oven. It makes sure the distribution is fair.

The Government Pension Offset (GPO):

This rule is for spouses, survivors, or even the workers themselves who receive a pension from a government job (like teaching in some states) where they didn't pay Social Security, and they are also eligible for Social Security benefits based on a spouse's or their own work in a Social Security-covered job.

The GPO works by reducing the Social Security spouse or survivor benefit by two-thirds of the amount of your government pension. So, if your pension is $1,500 a month, the GPO could reduce your spousal Social Security benefit by $1,000 (two-thirds of $1,500).

It's like having a discount coupon for your Social Security benefit. If you have a big pension from a non-Social Security job, the coupon might take a good chunk off your Social Security spouse benefit. It’s not that you don’t get anything, but the amount is adjusted.

Why Should You Care?

Okay, so why is this important for us everyday folks, even if we’re not retired teachers? Well, knowing these rules helps us plan for our own futures and the futures of people we care about. It's about making informed decisions, like choosing the right path on a hiking trail. You want to know where it leads!

For teachers themselves, understanding these provisions is crucial for retirement planning. It's like knowing how much gas is in the tank before you embark on a long road trip. You don't want to be surprised when you’re already on the way!

And for everyone else, it’s a good reminder that retirement planning isn’t a one-size-fits-all deal. Life throws curveballs, and so do retirement systems! Being aware of these nuances can help you offer support and understanding to friends or family members who might be navigating these situations. It fosters empathy, and a little empathy goes a long way, doesn't it?

So, to wrap it up with a warm hug: most retired teachers can collect Social Security, especially if they contributed to it during their careers. For those with pensions from non-Social Security jobs, the WEP and GPO might affect their benefits, but it doesn't necessarily mean they get nothing. It's all about understanding the system and planning accordingly. It’s like learning the rules of a new board game – once you get them, it’s much more enjoyable!